Melanocortin receptors (MC) are involved in the control of endocrine, autonomic and central nervous system functions. To date, five MC receptors subtypes have been identified. Targeting MC family of receptors provides therapeutic opportunities to treat a variety of conditions and diseases, including sexual dysfunction, obesity, cachexia (extreme wasting, generally secondary to a chronic disease) and inflammation. The 10Q Detective believes that MC-based therapeutics is one of the fastest growing areas of pharmaceutical research and development.

Palatin Technologies, Inc. (PTN-$2.58) is a biopharmaceutical company developing melanocortin-based therapeutics. The Company has a pipeline of product opportunities in late to early stages of development. To date, the Company has formed partnerships with Mallinckrodt, a subsidiary of Tyco Healthcare (TYC-$26.35), and King Pharmaceuticals (KG-$17.39).

NeutroSpec is the Company’s proprietary radio labeled monoclonal antibody product for imaging and diagnosing infection and is the subject of a strategic collaboration agreement with Tyco Healthcare Mallinckrodt. NeutroSpec was approved in July 2004 for use in the scintigraphic imaging of patients with equivocal signs and symptoms of appendicitis who are five years of age or older.

NeutroSpec includes a technetium-labeled anti-CD 15 monoclonal antibody that selectively binds to a type of white blood cell, neutrophils, involved in the immune response. When injected into the blood stream, the antibody binds to neutrophils present at the infection site, labeling these cells with a radioactive tracer. As a result, physicians can rapidly image and detect infection using a gamma camera, a common piece of hospital equipment that records radioactivity. Currently, this is [or was] the only significant revenue-generating stream for Palatin.

On December 19, 2005, Palatin and Mallinckrodt (sales and marketing partner) voluntarily suspended the sales of NeutroSpec and recalled all existing customer inventories. Palatin and Mallinckrodt acted at the request of the U.S. Food and Drug Administration (FDA). The decision to voluntarily suspend the sales, marketing and distribution of NeutroSpec followed the occurrence of several serious adverse events—including two deaths—in patients with severe underlying cardiopulmonary compromise who received NeutroSpec for off-label uses.

All ongoing clinical trials and regulatory approvals of NeutroSpec have been suspended. The Company and Mallinckrodt are reviewing data and assessing approaches for understanding the relationship between NeutroSpec use and the observed serious adverse events. The Company and Mallinckrodt are preparing for an FDA Advisory Committee meeting expected to be held later this year. As of April 2006, no final decision concerning future activities involving NeutroSpec has been made.

The Company’s internal research and development capabilities are anchored by its proprietary MIDAS technology. MIDAS is the first rational synthetic chemistry platform for the rapid conversion of peptides into therapeutics. MIDAS can quickly generate both receptor agonists (drugs that promote a particular response) and receptor antagonists (drugs that block a particular response), setting it apart from traditional combinatorial drug discovery methods. Key features of MIDAS are its ability to quickly and easily identify, and then stabilize, a desired conformation of a peptide for a specific drug target.

Bremelanotide (formerly PT-141), Palatin’s lead therapeutic candidate, is an MC receptor agonist, that has shown promise in effectively treating erectile dysfunction (ED) without the cardiovascular side effects found in ED drugs currently available (PDE-5 inhibitors). Bremelanotide is nasally administered, making it quick and easy to take and does not interact with other drugs, food or alcohol. According to published data, quality of erection, speed of onset, and duration of effect are what differentiate Bremelanotide from the PDE-5 inhibitor class of molecules. To date, Bremelanotide has been evaluated in four Phase 2 efficacy studies enrolling more than 300 men.

Of significance, too, was the fact that on February 8, 2006, the World Health Organization (WHO) formally recognized melanocortin agonists as a distinct therapeutic class and made Bremelanotide the first melanocortin agonist to have an approved generic name. The 10Q Detective believes that the formal recognition of the melanocortin pathway to modify biological processes validates MC-based R&D as an area worthy of big pharma interest (which will help Palatin facilitate future clinical partnerings).

Palatin is collaborating with King Pharmaceuticals to jointly develop and commercialize Bremelanotide in North America for both male and female sexual dysfunction. Financial terms of the collaboration are highly favorable to Palatin, with a potential for $250M in milestone payments and profit sharing on a worldwide basis. Under terms of the agreement, Palatin has retained the right to co-promote Bremelanotide to the urology specialty market and has operational responsibility for preclinical and clinical development and manufacturing, allowing Palatin to maintain a large interest in the value of the therapy.

In our last report, we mentioned that the current market for drugs to treat ED was estimated to grow from sales of US$3.8 billion in 2005 to approximately U.S.$6.6 billion by 2012. An even more sizable market exists in the treatment of female sexual dysfunction (FSD). According to the American Urological Association, more American women (43%; about 40 million) than men (31%) experience some form of sexual disorder, including both organic and psychogenic causes. Furthermore, the incidence of female sexual dysfunction increases after menopause when hormone production declines and neurovascular function is compromised. There are no FDA-approved medical treatments for FSD.

The Company is in the process of identifying a clinical candidate [MC therapeutic small molecule] for the treatment of obesity, and also has a program for the treatment of cachexia. The Company is also in the process of identifying a natriuretic compound for the treatment of congestive heart failure.

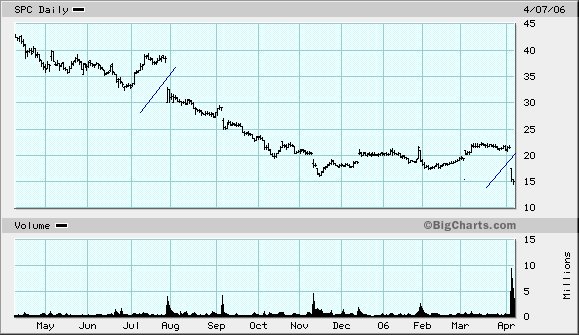

On April 17th the Company announced that it successfully closed on a stock/warrant offering that raised approximately $27.0 million in gross proceeds. The 10Q Detective estimates that with a monthly cash-burn rate pegged at about $2.8 million, Palatin currently has cash, cash equivalents and investments totaling approximately $25.0 million. The monthly cash-burn rate will obviously rise in the future as a result of spending on development programs. Nonetheless, management expects that existing cash reserves will be adequate to fund the Company’s operations for at least the next twelve months.

The near-term valuation of an emerging biotechnology company like Palatin is driven by the headlines. The share price will, therefore, be dependent upon the clinical success or failure of Bremelanotide.

Key factors in determining longer-term biotech valuations are time, cost, and peak sales/profitability estimates. The 10Q Detective believes that clinical development and approval by the FDA for Bremelanotide [in healthy males with mild-to-moderate ED] will take approximately five more years. The potential revenue stream to Palatin [less surrender value to manufacturing and marketing partners] could, in our estimates—top $2.0 billion annually (which includes off-label use in FSD, ‘lifestyle’ use, and co-use with PDE-5 agents).

According to historical industry standards, the odds of Bremelanotide’s ultimate success of moving through Phase III trials (balance between efficacy & safety) to market are about 67 percent. The risk-adjusted value of the revenue is 0.67 times $2.0 billion, or $1.34 billion. After discounting (at an internal rate of return of) 30.0%, using a price-sales ratio of 3, a trebling of shares outstanding to 180.0 million, our risk-adjusted 12-to-18-month price objective is $20.25 per share. Alternatively, an unsuccessful Phase III trial of Bremelanotide could depress the stock price to its cash value of $0.85 per share. BUY—but be aware.