’T is all men’s office to speak patience

To those that wring under the load of sorrow,

But no man’s virtue nor sufficiency

To be so moral when he shall endure

The like himself.

[Much Ado about Nothing. Act v. Sc. 1- William Skakespeare]

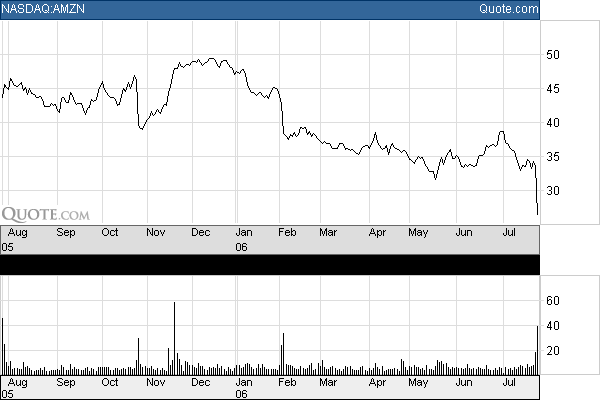

Weak results from Amazon.com Inc. (AMZN-$26.26) weighed heavily on trading Wednesday, as those investors of very melancholy disposition marched en masse to the exits, sending the shares down 21.82%, or $7.33 per share. The shares of the online retailer plummeted to a three-year low after the Company reported a 58% drop in second-quarter earnings and guided its full-year operating profits lower.

For the three months ended June 30, the Company reported a profit of $22 million, or 5 cents per share, compared with earnings of $52 million, or 12 cents per share in the prior year period, as higher operating costs offset a 22% rise in sales (to $2.14 billion).

Analysts polled by Thomson Financial were expecting second-quarter earnings of 7 cents per share on revenue of $2.1 billion.

Management cut its full-year operating income estimates to a range between $310 million and $440 million, down from a previous forecast of $390 million to $520 million.

In a conference call, management said operating income was hurt—and going forward into the 2H:06—margins will continue to be materially impacted, by the termination of the contract with Toys R Us Inc., the impact of free shipping promotions (for Amazon Prime club members), lower product prices, higher technology expenses, and the launch of new content (such as an online grocery store, toy store, and sporting goods store).

Piper Jaffray analyst, Safa Rashtchy, downgraded Amazon to under perform from market perform, saying that “while reduction of operating income guidance was expected, scope was larger than previously expected; it also takes Amazon further away from its goal of double-digit margins.” He cut his 66 cents 2006 EPS estimate to share-net of $0.55 and his 2007 EPS estimate from $0.96 to 86 cents. He also lowered his $38 stock price target to $25.00 per share.

Deutsche Bank analyst Jeetil Patel wrote in a note that while "overall investor sentiment surrounding the company (and its prospects) still appears to be acutely negative, we are nevertheless encouraged by some of the key trends in the 2Q results and momentum in the business."

Dan Geiman, an analyst at Seattle brokerage McAdams Wright Regan, noted that gross margins dropped 187 basis points to 23.8% from a year ago, cutting quarterly operating margins by more than half, to 2.2% from 5.9% in the second quarter of 2005. In a research note published Wednesday, he called margin pressures and earnings erosion "both worrisome trends" but took a wait-and-see stance, saying: "We expect that the stock may move sideways for the next quarter or two, but further expect that there is modest upside in the near to intermediate term if — and it's still a big if — AMZN can stem the tide and start to generate some earnings momentum.”

Perhaps Bear Stearns’ consumer Internet analysts said it best: The ultimate question has been and remains, “when will the necessary investing subside and when will the model begin to demonstrate the leverage that many believe can be achieved? While we believe investors will ultimately see these investments pay off, the waiting is the hardest part….”

Bear Stearns is reducing its 2006 Year-End Target Price from $47 to $40 per share, but is maintaining its ‘Outperform Rating.’

The confluence of events that conspired to drive down Amazon’s Common Stock price has inspired little confidence in the Company’s management—unfortunate to the credibility of the Wall Street analysts that are lowering their ratings & target price (after the stock has already plunged), and for the stockholders who will now have to wait even longer to see this investment “pay off.”

[Ed. note. “Even a dead cat will bounce if dropped from high enough!" To our readers expecting to trade off a potential bottom in Amazon, it is our view that any bullish rally will be short-lived, for the Common Stock still sells at a princely 30 times forward 2007 consensus EPS estimates.]

For the three months ended June 30, the Company reported a profit of $22 million, or 5 cents per share, compared with earnings of $52 million, or 12 cents per share in the prior year period, as higher operating costs offset a 22% rise in sales (to $2.14 billion).

Analysts polled by Thomson Financial were expecting second-quarter earnings of 7 cents per share on revenue of $2.1 billion.

Management cut its full-year operating income estimates to a range between $310 million and $440 million, down from a previous forecast of $390 million to $520 million.

In a conference call, management said operating income was hurt—and going forward into the 2H:06—margins will continue to be materially impacted, by the termination of the contract with Toys R Us Inc., the impact of free shipping promotions (for Amazon Prime club members), lower product prices, higher technology expenses, and the launch of new content (such as an online grocery store, toy store, and sporting goods store).

Piper Jaffray analyst, Safa Rashtchy, downgraded Amazon to under perform from market perform, saying that “while reduction of operating income guidance was expected, scope was larger than previously expected; it also takes Amazon further away from its goal of double-digit margins.” He cut his 66 cents 2006 EPS estimate to share-net of $0.55 and his 2007 EPS estimate from $0.96 to 86 cents. He also lowered his $38 stock price target to $25.00 per share.

Deutsche Bank analyst Jeetil Patel wrote in a note that while "overall investor sentiment surrounding the company (and its prospects) still appears to be acutely negative, we are nevertheless encouraged by some of the key trends in the 2Q results and momentum in the business."

Dan Geiman, an analyst at Seattle brokerage McAdams Wright Regan, noted that gross margins dropped 187 basis points to 23.8% from a year ago, cutting quarterly operating margins by more than half, to 2.2% from 5.9% in the second quarter of 2005. In a research note published Wednesday, he called margin pressures and earnings erosion "both worrisome trends" but took a wait-and-see stance, saying: "We expect that the stock may move sideways for the next quarter or two, but further expect that there is modest upside in the near to intermediate term if — and it's still a big if — AMZN can stem the tide and start to generate some earnings momentum.”

Perhaps Bear Stearns’ consumer Internet analysts said it best: The ultimate question has been and remains, “when will the necessary investing subside and when will the model begin to demonstrate the leverage that many believe can be achieved? While we believe investors will ultimately see these investments pay off, the waiting is the hardest part….”

Bear Stearns is reducing its 2006 Year-End Target Price from $47 to $40 per share, but is maintaining its ‘Outperform Rating.’

The confluence of events that conspired to drive down Amazon’s Common Stock price has inspired little confidence in the Company’s management—unfortunate to the credibility of the Wall Street analysts that are lowering their ratings & target price (after the stock has already plunged), and for the stockholders who will now have to wait even longer to see this investment “pay off.”

[Ed. note. “Even a dead cat will bounce if dropped from high enough!" To our readers expecting to trade off a potential bottom in Amazon, it is our view that any bullish rally will be short-lived, for the Common Stock still sells at a princely 30 times forward 2007 consensus EPS estimates.]

1 comment:

Very interesting article.

Post a Comment